What Does Liability Cover?

Liability Coverage is the glue that holds our streets together. I mean just think about it - we let 3000 pound cars fly down the freeway in a V formation 12 feet away from each other separated by painted dashes on the ground. Any one person's mistake or intrusive thought can cause $100,000's of dollars in physical damage and millions in pain & suffering.

And I don't know about you, but me and everyone I know cannot pay for damages that high out of our own pocket. What keeps everybody on the street is the TRUST that any accidents that happen will be compensated to the point that the people injured and property destroyed are "Made Whole".

And that's what liability coverage does... kind of.

How We Talk About Liability

Liability maximums are written in 3 numbers, like 100/250/50.

- the 1st number is the max a single person could be paid for injuries by your insurance ($100,000)

- the 2nd is the max paid out in bodily injury payments to all persons in an accident ($250,000)

- the 3rd is the max your insurance will pay out in physical property damage for people's cars ($50,000)

Hearing that there is a maximum that your insurance will pay for an accident, the natural question is: "What happens if the accident I caused costs more than that?".

Well, what definitely doesn't happen is the insurance company paying a single cent more than that maximum. When that max is hit, their contractual obligation to cover you is done and they are NOT budging.

The other party or parties in that accident only have one choice, and that's to sue you personally and go after your assets and future income.

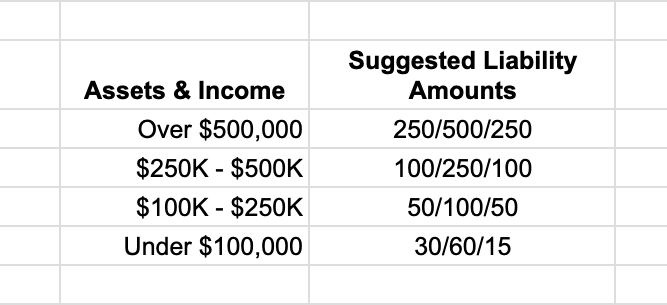

So How Much Liability Should I Get?

Since the first thing someone who runs into your insurance liability maximums will do is sue you, the first question is, do you have anything they can collect? Very important note: they are unable to go after your 401k so don't include that in your assessment.

So if you have a high-paying job, or assets like a house or investments, then you'll want to get enough to protect that income and assets.

Since we are trying to forecast something in the future that has not happened yet, everything's a guess, but in general this is what we suggest:

These are just guidelines of course. If you want to have more or have less because of how conservative or not conservative you want to be.

There are also some rogue suggestions we might recommend. For example if you drive a really nice car we'd suggest to have as much liability as possible - since anyone you run into is most likely getting a personal injury lawyer immediately.